-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Smart Minor (Joint) Account

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

李曉然小姐(Margaret Li)

分析師

分析師

本科主修市場行銷和英語,並於香港浸會大學獲得經濟學碩士學位。現為輝立証券持牌分析師,主要負責能源和公用事業等板塊的研究。曾在大型銀行、券商和資產管理公司工作,對於期貨和大宗商品衍生品領域擁有銷售、研究分析和市場推廣等工作經驗。

Margaret, a holder of a Bachelor`s degree in Marketing and English and a Master`s degree in Applied Economics from Hong Kong Baptist University, is currently employed as a licensed analyst at Phillip Securities. She specializes in conducting research focusing on the energy and utilities sectors. Prior to her current position, Margaret gained valuable work experience in a large bank, securities firm, and asset management companies. Her expertise lies in sales, research analysis, and marketing within the fields of futures and commodities derivatives.

| Phone: | 22776535 | Email: | margaretli@phillip.com.hk | |

Lafang China (603630.CH) - Sales expenses increased significantly, and we expect the volume to increase gradually in the future

Monday, June 23, 2025  607

607

Lafang China(603630)

| Recommendation | Neutral |

| Price on Recommendation Date | $23.940 |

| Target Price | $24.650 |

Weekly Special - 1810 Xiaomi

Leading Company of national brand shampoo

Lafang China Co., Ltd is a personal care product enterprise integrating R&D, production, sales and independent brands, and is one of the leading domestic brands of shampoo. The company owns shampoo and hair care, cleansing and bathing, skin care, and oral care brands such as Lafang, Mese, Raclen, Taoran, Mansina, Jiaocaotang, Binchun, Saint Peak, and Baixiaoqi.

Sales expenses increased significantly in 2025Q1, and we expect the volume to increase gradually in the future

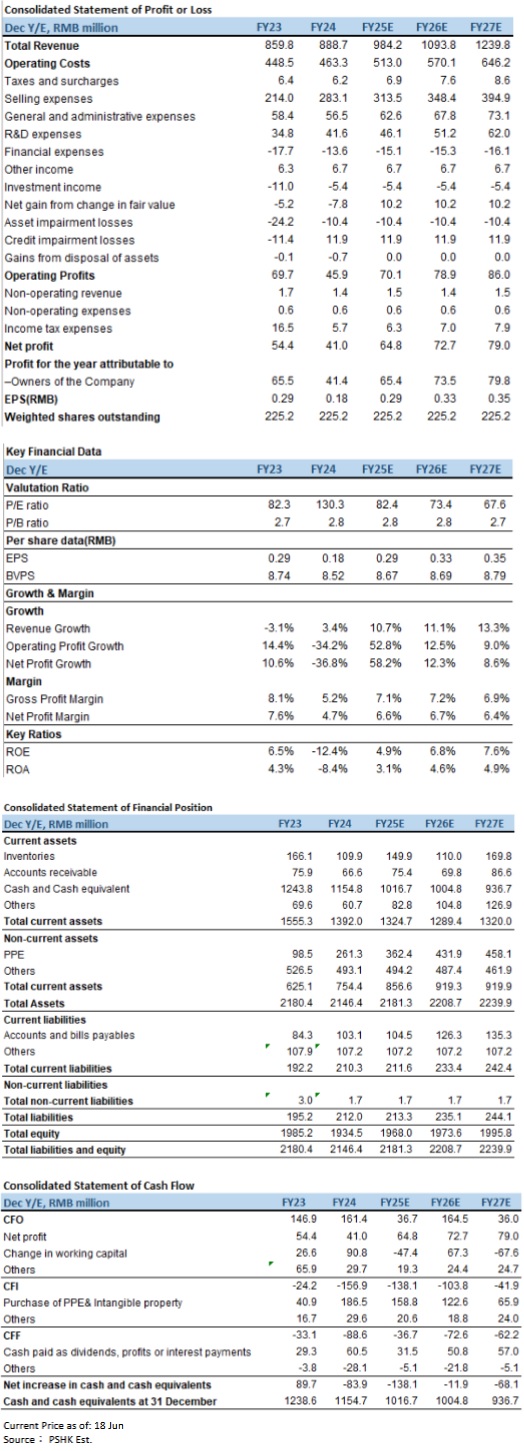

In 2025Q1, the company's operating revenue was 210 million yuan (RMB, the same below) with a year-on-year decrease of 6.27%; sales expenses were 67 million yuan with a year-on-year increase of 22.55%; net profit attributable to shareholders was 13 million yuan with a year-on-year decrease of 53.30%, mainly due to the increase of the company's e-commerce traffic costs, advertising and promotion expenses during the reporting period; net cash flow from operating activities was 36 million yuan with a year-on-year decrease of 64.87%, mainly due to the decrease in cash received from the sale of goods and provision of services in this period and the increase in payments of other expenses relating to operating activities; EPS was 0.06 yuan with a year-on-year decrease of 50%.

In 2024, the company's operating revenue was 889 million yuan with a year-on-year increase of 3.36%. By brand, "Lafang" and " Raclen " are still the company's pillar brands, accounting for 88.57% of the revenue, of which "Lafang" sales revenue was 641.62 million yuan with a year-on-year increase of 9.11%; " Raclen " sales revenue was 145.47 million yuan with a year-on-year increase of 27.98%. By channel, the distribution channel is still the company's main sales channel, accounting for 70.11% of the revenue, with revenue of 623.12 million yuan with a year-on-year increase of 4.42%; e-commerce and other channels achieved operating revenue of 264.88 million yuan with a year-on-year increase of 2.73%, proving that the company's e-commerce and other channel revenue still has a lot of room for improvement. As the company increases its investment in e-commerce platforms such as Douyin, Tmall, and JD.com and it has launched hot products about hair core repair, dandruff removal, anti-hair loss and improving hair growth, which will help the company open up a new growth situation for the online channel and promote the growth of the company's e-commerce channel revenue. Sales expenses were 283 million yuan with a year-on-year increase of 32.27%, resulting in a net profit of 41 million yuan attributable to the parent company with a year-on-year decrease of 36.84%; net cash flow from operating activities was 161 million yuan with a year-on-year increase of 9.94%, and EPS was 0.19 yuan with a year-on-year decrease of 34.48%.

Cultivating the hair care field deeply while enriching the product matrix

Lafang China was founded in 1997 and launched a series of soap products the following year. In 2001, Lafang China launched a double-layer care and smooth shampoo. The slogan "Love life, love Lafang" was very popular at the time, which effectively expanded the company's brand influence. Over the years, the company has continued to deepen its roots in the hair care field. Its current independent care brands mainly include "Lafang", " Raclen" and " Mese". The company implements a precise positioning strategy for care brands. "Lafang" focuses on smooth care, " Raclen" focuses on professional dandruff removal, and aims at high-speed rejuvenation. It signed Wang Yuan as a spokesperson to promote penetration into young customer groups, while " Mese" is an essential oil care brand for the high-end market. At the same time, the company actively explores the field of skin care. In the second half of 2024, the first product "Lafang Anti-Wrinkle Firming Rejuvenating Cream" was successfully launched which meant the layout in the skin care field had begun to show results. In addition, the company introduced the German professional clinic skin care brand " REPACELL". In 2025, " REPACELL" will continue to consolidate its position in the high-end skin care field.

Layout of medical beauty track to find new growth points

In April 2025, Lafang China invested 3.5 million yuan in Peptide Source (Guangzhou) Biotechnology Co., Ltd., holding 18.78% of the shares, making itself become the company's second largest shareholder. Peptide Source Biotechnology was established in 2017, and it is a company specializing in R&D, production and sales of biologically active functional raw materials, cosmetic raw materials, and medical device excipients. The company takes recombinant protein active peptides, microbial fermentation, liposome encapsulation and microemulsification application technology as the three main research and development lines. At the same time, it is also committed to the development of high-end preparation application technologies such as raw material activity maintenance, transdermal absorption, and sustained release. It has microfluidics, microfluidics production lines, raw material freeze-dried preparation production lines, and 100,000-level GMP workshops. At present, the company has research and development and production equipment worth nearly 30 million yuan. Recombinant protein active peptides have a wide range of application scenarios in the fields of skin beauty and anti-aging and have broad development prospects. The company developed a variety of masks (such as Peptide Source Mechanical II Crystal Mask, Peptide Source Class II Medical Device Grade "Wound First Aid Cream", etc.) which can be used in the field of medical beauty repair. The investment means that the company is actively developing its presence in the medical beauty sector and working hard to find new business growth points.

Deeply integrating industry, academia and research to actively enhance R&D capabilities

In 2025, Lafang launched the sixth generation of smart peptide hair core repair technology, focusing on 360° repair of scalp-hair-hair core, and won the world record certification of "hair resisting 1 million stretching after washing and care", strengthening the technology label. In March this year, the "Key Technology Research and Development of Natural Characteristic Functional Hair Care Raw Materials" project of Lafang International Daily Chemical Research Center made a breakthrough. Lafang enriched the high content of active polysaccharides from orchid plants, and tests showed that it had strong antioxidant properties. It can be applied to cosmetics and can provide skin conditioning and anti-aging protection. The company continued to increase its R&D investment. In 2024, the R&D investment was 42 million yuan with a year-on-year increase of 19.59%, and the R&D expense rate was 4.68%. The company had established extensive cooperative relations with domestic and foreign scientific research institutions to build an innovative ecosystem of "basic research-technology development-industrial application". Although Lafang China attaches great importance to R&D, taking a closer look at the academic structure of its R&D personnel (taking 2024 as an example), we will find that the proportion of doctoral and master's degree scientific researchers only accounted for 1%, and the technical reserves were slightly weak.

Collaborating with Huawei and China Mobile and using DeepSeek to enable digital intelligence upgrades

In February 2025, the launch ceremony of the comprehensive cooperation jointly held by Lafang China, Huawei and China Mobile was grandly opened, and the Lafang AI digital intelligence platform was officially launched with DeepSeek. This marked a key step for Lafang China in the construction of smart factories and digital transformation. This cooperation and the involvement of DeepSeek will help Lafang China optimize the entire chain of R&D, production, sales and supply.

Investment Thesis

As a long-established domestic hair care company, Lafang China faces fierce competition and transformation pressure. Starting from 2024, Lafang China was ready to go, focusing on brand reshaping in the field of hair care and striving to achieve sales breakthroughs. In March 2025, it signed a contract with the Chinese National Diving Team (Quan Hongchan, Chen Yuxi, etc.) and launched a new positioning of "China Lafang, the Choice of Champions". Through the endorsement of the diving team and live broadcast activities, Douyin sales soared in the short term. The company plans to continue to tap into traffic benefits through 24-hour regular live broadcasts and matrix account operations and hopes it become a new revenue engine. However, the company's sales expenses increased significantly, and net profit was under pressure in the short term. We expect that the volume will increase gradually in the future, and it can result in a substantial increase in online revenue to reverse the downward trend. In addition, if the company's subsequent layout of the medical beauty area makes progress, it is expected to become a new growth point for the company's revenue. However, if the company's online sales only increase in the short term and slow down later, it may fall into a situation of "more revenue but less profit".

We forecast that the company's operating revenue will be RMB 0.98 billion, RMB 1.1 billion and RMB 1.2 billion in 2025-2027, with EPS of RMB 0.29/0.33/0.35, corresponding to a price-earnings ratio (P/E) of 82.4x/73.4x/67.6x respectively. We assign a target price of RMB 24.65, based on 85x FY2025E P/E, and give it a "Neutral" rating for the first time. (Current price as of Jun 18)

Risk factors

Downward macroeconomic situation, intensified industry competition, management changes, and new product promotion failing to meet expectations.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()